[ad_1]

If you’re in the market for a personal loan — also called an installment loan — in 2022, expect to pay a higher interest rate than you would for a mortgage or auto loan.

At the beginning of 2022, personal loan rates averaged a little more than 10%. That’s still better than the average interest rate of a credit card, which WalletHub estimates at more than 18%.

In this article, we’ve highlighted the best installment loans available on the market, prioritizing those installment loans that had low annual percentage rates (APRs), affordable monthly payments, low credit score thresholds and flexible loan amounts and repayment terms.

Contents

What Is an Installment Loan?

At a high level, an installment loan is a lump sum of cash that you borrow from a lender for a specific project or opportunity, with clear stipulations for paying back that money, plus interest, over a set amount of time.

In that way, auto loans, mortgages and student loans are considered installment loans, but lenders typically offer specific programs for those kinds of loans. Instead, most borrowers equate installment loans with personal loans for things like home renovations, a wedding, an emergency or even debt consolidation.

Installment loans differ from credit cards (a form of revolving credit) in that you borrow a specific, one-time amount from the lender and agree upon a payoff term, meaning you will have set monthly payments (or installments) of a predictable amount until you have paid off the loan amount in full.

Though each loan is different, typical terms range from 12 months to 96 months — that’s one to eight years.

Best Installment Loans of April 2022

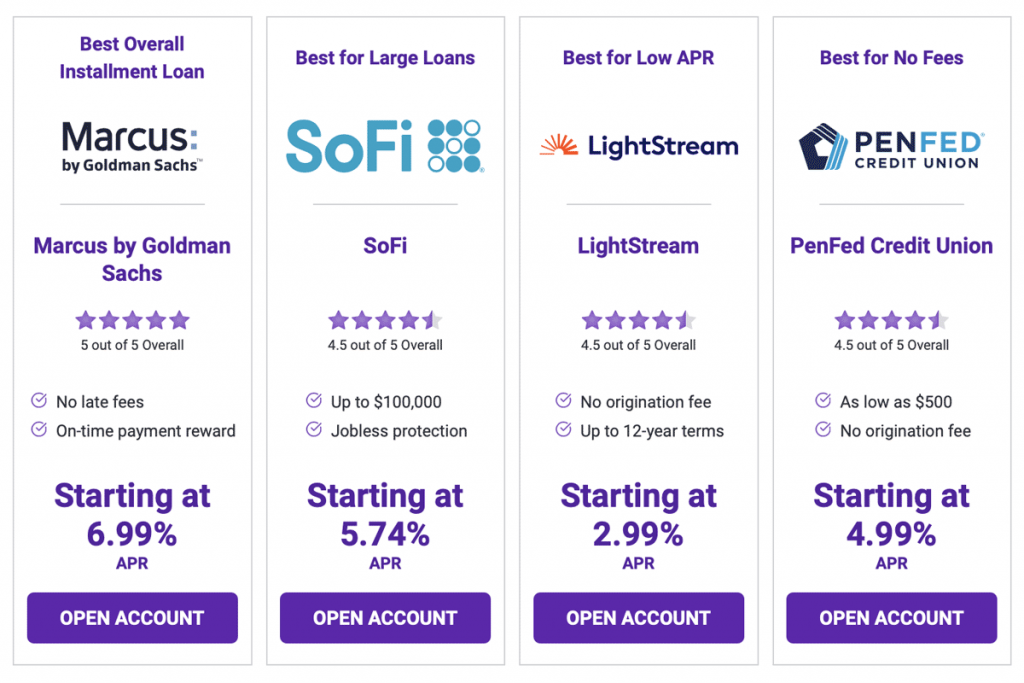

Marcus by Goldman Sachs

Best Overall Installment Loan

Key Features

- No late, prepayment or origination fees

- On-time payment reward

- Favorable APR range

Marcus by Goldman Sachs is the gold standard for personal loans. You don’t need to sweat origination fees, prepayment penalties or even late fees. But if you’re a master of on-time payments, you’ll secure a reward: Pay your monthly installment in full and on time for 12 consecutive months, and you can skip the next month, without interest.

Marcus by Goldman Sachs

APR range

6.99% to 19.99% with auto pay

Loan amount

$3,500 to $40,000

Minimum credit score

600

Origination fee

$0

Loan terms

3 to 6 years

Let’s weigh the pros and cons of installment loans with Marcus by Goldman Sachs:

Pros

- No origination fee

- No prepayment penalty

- No late fees

- On-time payment reward (defer payment)

- APRs capped at 19.99% on the high end

Cons

- High minimum credit score threshold

- Low max loan amount

- Up to four days for funding

Final Thoughts: Marcus by Goldman Sachs is our top choice for personal installment loans. While it caters to borrowers with stronger credit scores, its lack of fees, rewards for on-time payments and low APRs make it ideal for everything from home improvement loans to debt consolidation loans. We just wish the max loan amount was a little higher.

SoFi

Best for Large Loans

Key Features

- Unemployment protection

- Same-day funding

- Up to $100,000 for personal loans

SoFi offers one of the best installment loans on our list, thanks to its flexible use cases (shout-out to SoFi for listing IVF), same-day funding, lack of prepayment and origination fees, impressive APR range and large max loan amount. But the standout feature is its unemployment protection.

SoFi

APR range

5.74% to 21.78% with auto pay

Loan amount

5,000 to $100,000

Minimum credit score

Not disclosed

Origination fee

$0

Loan terms

2 to 7 years

Let’s weigh the pros and cons of installment loans with SoFi:

Pros

- No origination fee

- No prepayment penalty

- Wide loan term range

- Same-day funding

- Unemployment protection

Cons

- Credit score requirement not disclosed

- Not flexible for smaller loans

Final Thoughts: If you’re looking for an installment loan with no fees, same-day funding and unemployment protection, SoFi is one of the top options. Plus, you can borrow up to $100,000, which makes SoFi great not just for debt consolidation loans but also major home renovations. The minimum loan amount might be the only deal-breaker for some borrowers.

LightStream

Best for Low APR

Key Features

- Lowest APR available

- Same-day funding

- Long repayment terms available

LightStream has the lowest fixed interest rate on the list and also one of the longest repayment terms on the market at up to 12 years. We also like the competitive interest rates across the board — APRs are capped at 19.99%. You can get same-day funding with LightStream for a loan up to $100,000, and there is no origination fee or prepayment penalty.

LightStream

APR range

2.99% to 19.99% with auto pay

Loan amount

$5,000 to $100,000

Minimum credit score

Not disclosed

Orgination fee

$0

Loan terms

2 to 12 years

Let’s weigh the pros and cons of installment loans with LightStream:

Pros

- No origination fee

- No prepayment penalty

- Flexible repayment terms (up to 12 years)

- Same-day funding

- Easy-to-use app

Cons

- Credit score requirement not disclosed

- Not flexible for smaller loans

Final Thoughts: LightStream has the lowest APR of any of the online installment loans on our list, which makes it worth consideration for anyone shopping for an installment loan. While LightStream is good for debt consolidation and major renovations, it’s also a great option for emergencies since they offer same-day funding.

PenFed Credit Union

Best for No Fees

Key Features

- Loans as small as $500

- No hidden fees

- Favorable APR terms

PenFed Credit Union benefits from the federal cap on credit union APRs (18%) for installment loans, giving it the lowest max APR for personal loans. There are also no origination or prepayment fees with PenFed, and you can get loans as brief as a single year for as little as $500.

PenFed Credit Union

APR range

4.99% to 17.99% with auto pay

Loan amount

$500 to $50,000

Minimum credit score

700

Origination fee

$0

Loan terms

1 to 5 years

Let’s weigh the pros and cons of installment loans with PenFed Credit Union:

Pros

- No origination fee

- No prepayment penalty

- Short repayment terms available

- Low loan amounts

- he best APR max on the list

Cons

- Have to become a PenFed Credit Union member

- 1 to 2 business days for funding

Final Thoughts: While you’ve got to join the credit union to be eligible for the loan, that’s not a bad thing. An online bank account may offer the best features, but compared to brick-and-mortar banks, credit unions more often offer better rates and features.

Upgrade

Best for Bad Credit

Key Features

- 560+ credit score required

- One-day funding

- Small loan options

Upgrade’s $1,000 threshold for loans make the online lender a top choice for more than just medical emergencies; it’s also a great option for small household purchases like furniture and appliances. We like the fast funding, even for borrowers with bad credit scores, but borrowers should be wary of the APR, which can creep into the high 30s.

Upgrade

APR range

5.94% to 35.47% with auto pay

Loan amount

$1,000 to $50,000

Minimum credit score

560

Origination fee

2.8% to 8%

Loan terms

3 to 5 years

Let’s weigh the pros and cons of installment loans with Upgrade:

Pros

- No prepayment penalty

- One-day funding

- Low loan amounts

- Low credit score requirement

Cons

- Potentially high origination fee

- High max APR

Final Thoughts: Upgrade offers one of the best installment loans for bad credit, requiring only a 560 credit score. Plus, with $1,000 loans and one-day funding, Upgrade is practical for life’s big and little purchases. We’re not huge fans of origination fees, and be cautious of the potentially high APR.

LendingClub

Best for Small Loans

Key Features

- 600+ credit score required

- 15.95% average APR

- Small loan options

LendingClub ticks a lot of boxes if you’re looking for an installment loan. You can get a small loan of just $1,000, there’s a low minimum credit score requirement (600) and there are no prepayment penalties. But the low end of the APR range falls at 7.04% (let’s not talk about the 35.89% on the other end), and the origination fee and 48-hour funding time are not ideal.

LendingClub

APR range

7.04% to 35.89%

Loan amounts

$1,000 to $40,000

Minimum credit score

600

Origination fee

3% to 6%

Loan terms

3 or 5 years

Let’s weigh the pros and cons of installment loans with LendingClub:

Pros

- No prepayment penalty

- Low loan amounts

- Low minimum credit score requirement

Cons

- Potentially high origination fee

- High minimum APR

- High max APR

- 48-hour funding period

- Inflexible loan term options

Final Thoughts: LendingClub does a few things right, like its small loan amount options and low credit score requirement. But be aware of its high APR range, stiff loan term options and high fees and long funding period.

Best Egg

Best for Customer Satisfaction

Key Features

- 600+ credit score required

- Leading customer reviews

- Small loan options

Best Egg has the highest max APY, stiff loan term options (3 or 5 years) and an origination fee. However, Best Egg has amazing reviews with BBB and TrustPilot, so customers are certainly satisfied. The 600 minimum credit score is also good for borrowers struggling with a bad credit score.

Best Egg

APR range

5.99% to 35.99%

Loan amount

$2,000 to $50,000

Minimum credit score

600

Origination fee

0.99% to 5.99%

Loan terms

3 or 5 years

Let’s weigh the pros and cons of installment loans with Best Egg:

Pros

- No prepayment penalty

- Low minimum credit score requirement

- Great customer reviews

Cons

- Potentially high origination fee

- High max APR

- Unclear (but lengthy) funding period — multiple days

- Inflexible loan term options

Final Thoughts: What Best Egg does really well is take care of its customers. Whether through strong customer support or inclusive communication efforts, something has struck a nerve with their customers. For many, that makes up for less than favorable loan terms, an only moderately sized max loan amount, potentially high APR and long funding period.

Upstart

Best for Insufficient Credit History

Key Features

- 300+ credit score required

- Also approves w/ insufficient credit history

- Small loan options

Upstart offers the best installment loans for borrowers who haven’t yet established a credit history. And with an acceptance of borrowers with credit scores as low as 300, Upstart also offers the best personal loans for bad credit. We don’t love the origination fee (up to 8%), and while APRs start as low as 3.09%, borrowers with bad credit (or no credit report) can expect to pay up to 35.99%.

Upstart

APR range

3.09% to 35.99%

Loan amount

$1,000 to $50,000

Minimum credit score

300 (or insufficient credit history)

Origination fee

0% to 8%

Loan terms

3 to 5 years

Let’s weigh the pros and cons of installment loans with Upstart:

Pros

- No prepayment penalty

- Low minimum credit score requirement

- Loan options for those with no credit history

- Next-day funding

Cons

- Potentially high origination fee

- High max APR

- Inflexible loan term options

Final Thoughts: Hands down, Upstart offers the best bad credit installment loans, allowing borrowers with scores as low as 300 — or no credit report at all. Unfortunately for those borrowers, who don’t have many options, that means high APR and plenty of fees.

Avant

Best for Mobile Users

Key Features

- Next-day funding

- 580+ credit score required

- Highly rated mobile app

With a low minimum credit score requirement of just 580, Avant offers one of the best installment loans for bad credit. However, its low end of the APR range (a whopping 9.95%) reflects that this is for borrowers who have few options. The origination fee (called an administration fee) is another ding for Avant, but mobile users will appreciate how easy to use the app is. It has high scores on the Apple App Store.

Avant

APR range

9.95% to 35.99%

Loan amount

$2,000 to $35,000

Minimum credit score

580

Origination fee

4.75%

Loan terms

2 to 5 years

Let’s weigh the pros and cons of installment loans with Avant:

Pros

- No prepayment penalty

- Low minimum credit score requirement

- Highly rated mobile app

- Next-day funding

Cons

- High origination fee (administration fee)

- High starting APR

- High max APR

Final Thoughts: Avant’s mobile app is its saving grace, but in terms of APR, fees and flexible loan terms, it can’t compete with some of our top-of-the-list options. Avant does, at least, cater to borrowers with poor or fair credit, making it one of the better installment loans for bad credit.

Types of Installment Loans

While those shopping for installment loans are typically looking for personal loans, installment loans technically refer to a fixed-interest rate loan with regular monthly payments. In that way, auto loans, mortgages and student loans are also considered installment loans.

Unlike typical personal loans, vehicle loans and home loans, student loans often have a variable interest rate. Payments can change over time, based on your income, family size and other factors.

Auto and home loans are considered secured loans, meaning they require collateral. Because personal loans, which are unsecured loans, do not require collateral, interest rates are higher.

3 Reasons for Getting a Personal Installment Loan

While you can get a personal loan for anything, like a vacation or a wedding, taking on debt with such a high interest rate should be done cautiously. We recommend taking out a personal loan only if you already have flexibility in your monthly budget to handle the additional monthly installment payments at your current income.

There are three main scenarios for which we consider taking out a personal loan:

1. For a Relatively Safe Long-Term Investment

Renovating your home, whether it’s a small project or complete home makeover, is expensive, but we can usually expect to get out more than we put into our homes, if the market is decent.

You have multiple options for financing major renovations, including refinancing your mortgage; taking out a home equity line of credit (HELOC), which is a secured loan; or taking out a home equity loan. But while you’re weighing out your options, you can also consider a personal loan for home repair or home improvement. Just be sure that whatever you’re putting into the home, plus the interest you’ll pay on the loan, is less than what you’ll get out of the house when you sell it.

You might also consider an unsecured loan if you are launching your own small business but can’t qualify for a traditional business loan.

2. To Consolidate your debt

If you are drowning in credit card debt on multiple cards — and struggling with their varying due dates, minimum payment amounts and APRs — taking out a fixed-rate personal loan with a monthly installment plan to pay off those credit cards can be a wise idea. Typically, the interest rate on such an installment loan will be lower than any of the credit cards you’re juggling, and you’ll only have one monthly due date to juggle.

3. In an Emergency

According to a 2021 survey by SSRS Omnibus, more than half of Americans have less than three months’ worth of emergency savings in their bank accounts — while many experts say we need double that. If you find yourself faced with an emergency medical bill or suddenly in need of cash, a personal loan might be your best bet.

If you can get access to one quickly, preferably the same day, an installment loan is a better idea than racking up credit card debt in these scenarios.

How to Get the Best Installment Loan

When looking for a personal loan, always review multiple options. However, you want to avoid having too many lenders pull your credit, as multiple hard inquiries can have a (temporary) negative effect on your score.

That’s why it’s important to skim rankings of the best installment loans, like we’ve provided above. This allows you to compare multiple options without actually applying. Just note that your particular situation might yield different results from what we reviewed above.

Nowadays, many online lenders can also provide estimated loan terms without pulling your credit.

Key elements of the best installment loan include:

- Lack of fees (no origination fee, no prepayment penalties and no late fees)

- Low APRs

- Flexibility around loan amount and loan terms

- Options for fair credit or bad credit

- Bonus features, like on-time payment rewards and unemployment protection

If you are looking specifically for loans for bad credit, lower your expectations around fees, APRs and flexibility. But if at all possible, do not humor a payday loan — a predatory loan that takes advantage of borrowers with bad or fair credit in emergency situations.

Some lenders only consider your credit score when making an approval decision, but other lenders may consider elements like debt-to-income ratio, assets and payment history.

Where to Get an Installment Loan

When shopping for installment loans, you can consider banks, credit unions and online lenders. Keep all of these options in mind when trying to find the best installment loan, prioritizing the lowest rates, the most affordable monthly payments and the best terms and features for your scenario.

Banks

If you already belong to a national bank, start your search here. Valued customers at larger banks can often get lower rates just for having active checking or savings accounts or other loan products.

Credit Unions

Similarly, if you are a member of a specific credit union, you can likely qualify for a reduced rate on your unsecured personal loan. Even if you don’t belong to a credit union, consider getting your installment loan from one. Federal credit unions are capped at 18% APR for personal loans; even at the maximum, that’s lower than the average credit card APY.

Online Lenders

The nice thing about some (not all) online lenders is that they allow you to pre-qualify before you apply. This enables you to review multiple online lenders without a hard inquiry on your credit.

Borrowers with bad credit scores will have more luck with online lenders than at banks and credit unions. However, be cautious: Though online lenders do cater to those with bad credit scores, the resulting interest rate can be incredibly high.

How Installment Loans Affect Your Credit Score

As mentioned above, applying for any kind of loan, including a personal loan, will result in a hard inquiry. This temporarily lowers your credit score, but it’s such a small factor in the grand scheme of things — and just a necessary evil of the loan process — that you shouldn’t sweat it too much.

But can installment loans affect your credit score in positive ways? Yes — if you make your payments on time. Credit bureaus love to see a long history of on-time payments, so the longer you have the installment loan account open with on-time payments, the higher your score will climb. When you eventually pay off the loan, you might see a nice bump in your score as well; credit bureaus also look for evidence that you can pay debt to completion.

Frequently Asked Questions (FAQs) About Installment Loans

Still have questions about installment loans? We’ve taken the most common questions readers are asking and provided some quick answers. See if we’ve addressed your question below:

What Credit Score Do I Need for an Installment Loan?

This varies by lender. Some of the best installment loans on our list have no minimum credit score requirement while others require scores somewhere in 500s or even 600s. You can expect better rates with a higher credit score, but if you do have a low credit score, there are options available to you.

If you cannot find a suitable installment loan, there are no-credit-check lenders offering payday loans, but we strongly urge caution when considering these.

Can I Pay Off an Installment Loan Early?

You can pay off an installment loan early, but this won’t have a major effect on your credit score. Paying it off early can, however, save you money on interest. If you pay off the loan several years early, this can bring you significant savings. But be cautious: Some installment loans have prepayment penalties. When looking for the best installment loans on offer, check the fine print for such penalties; if you hope to be able to pay off your loan early, avoid any offers that will charge you this fee.

Are Installment Loans Secured or Unsecured?

Installment loans is a blanket term that covers any kinds of loans that allow you to borrow a lump sum and pay it back in agreed upon monthly installments over a set number of months. Within this broad category, there are both secured loans and unsecured loans. A secured loan is one for which you must provide collateral, like an auto loan or a mortgage. Because of this collateral, lenders can offer lower interest rates for a secured loan. Personal loans are unsecured loans. You do not need to provide collateral, but interest rates will be higher as a result.

Can I Have Multiple Installment Loans?

Yes, you can have multiple installment loans at once. You might have a mortgage, car loan and a personal loan — or even multiple personal loans. Just be careful: Unlike revolving credit, there is no minimum payment option. You are on the hook each month for the full monthly installment.

What Happens if I Default on an Installment Loan?

Unlike credit cards, which allow you to make a low monthly minimum payment and carry debt from month to month, personal loans require you to pay a standard amount each month. If you are more than 30 days late for a payment (some lenders are more forgiving), you can be considered in default on that loan. When this happens, the lender will likely send your loan to collections, and your credit score will be negatively affected. You can also expect to owe late fees. If the installment loan is unsecured, there is no collateral for the lender to seize, so the lender may take you to court and ultimately garnish your wages or place a lien on your assets.

Can I Get an Installment Loan With Bad Credit?

Yes, multiple lenders offer bad credit installment loans. If you do have bad credit, you’ll just encounter higher fees and interest rates.

What Are Auto Pay Discounts?

Many installment loans offer a slightly lower APR (usually 0.25%) if you set up auto pay. This means your monthly installment will debit directly from your bank account each month. It’s a win-win; the online lender doesn’t have to hunt down the money it is owed, and you don’t have to sweat late payments (and fees). Just make sure you have enough in your checking to cover the withdrawal each month.

How Are Installment Loans Different From Payday Loans?

A payday loan is quite different from an installment loan. While installment loans allow you to make regular payments (i.e., installments) over a set period of time, payday loans require that you pay the lender back on your next payday. Because payday loans are designed for borrowers with no credit or bad credit, the terms are never favorable and can land borrowers in a deep financial hole. If you can, avoid taking out a payday loan at all costs.

How Are Installment Loans Different From Credit Cards?

Credit cards are a revolving credit: You can borrow money as you need and make payments as you are able, as long as you are making the minimum payment each month. Because this makes it easier to spend money you don’t have, credit cards have much higher APRs. Installment loans are much more structured: You borrow a lump sum amount and then have a solid repayment plan over a set number of months.

How Does Debt Consolidation Work?

Debt consolidation allows you to take multiple debts you are juggling (usually from various credit cards or multiple student loans) and wrap all those debts (i.e., consolidate debt) into one larger debt. The lender will pay off your outstanding debts, and now you will manage a single monthly payment with that new lender. You can also consider a balance transfer credit card as a debt consolidation tactic.

Timothy Moore covers banking and investing for The Penny Hoarder from his home base in Cincinnati. He has worked in editing and graphic design for a marketing agency, a global research firm and a major print publication. He covers a variety of other topics, including insurance, taxes, retirement and budgeting and has worked in the field since 2012.

[ad_2]