[ad_1]

Student loan repayment dampens the financial plans of a lot of people in this country. The federal government may be on the brink of major plans to lessen that burden for public loan borrowers — but if you’re paying off private student loans, you’re still on the hook.

Student loan refinancing consolidates federal and private student loans to bring everything into one simple monthly payment, potentially reduce your interest rate and/or monthly payment, and adjust your repayment term to better suit your needs.

We reviewed the best student loan refinance companies to help you see your options in one place and find the option that’s best for your financial circumstances.

This post includes more details on every lender, plus all the information you need to find the best student loan repayment plan for you.

Interest rates are accurate as of May 2022 and subject to change. Variable rates listed are margins added to a base rate such as LIBOR or SOFR, which could add around 0.30% to 1%.

Best Student Loans at a Glance

| Lender | Variable APR with Autopay | Fixed APR with Autopay | |||

|---|---|---|---|---|---|

| Credible | 1.86% – 8.38% | 2.35% – 8.73% | SEE DETAILS | ||

| Earnest | Starting at 1.74% | Starting at 2.74% | SEE DETAILS | ||

| College Ave | 3.44% – 6.64% | 3.49% – 6.74% | SEE DETAILS | ||

| SoFi | 1.74% – 7.99% | 3.49% – 7.99% | SEE DETAILS | ||

| LendKey | Starting at 2.14% | Starting at 2.69% | SEE DETAILS | ||

| Citizens Bank | Starting at 1.99% | Starting at 3.75% | SEE DETAILS | ||

| PNC Bank | 2.14% – 6.64% | 2.59% – 7.19% | SEE DETAILS | ||

| Purefy | 1.74% – 7.24% | 2.43% – 7.94% | SEE DETAILS | ||

| Sparrow | 1.74% – 9.34% | 2.35% – 10.74% | SEE DETAILS | ||

| Discover | 1.79% – 11.09% | 3.49% – 7.99% | SEE DETAILS | ||

| Splash Financial | 1.74% – 8.70% | 1.99% – 8.63% | SEE DETAILS | ||

| ISL Education Lending | n/a | 4.10% – 7.86% | SEE DETAILS | ||

| Laurel Road | 1.89% – 6.20% | 2.99% – 6.30% | SEE DETAILS | ||

| PenFed Credit Union | n/a | 4.49% – 6.68% | SEE DETAILS |

Contents

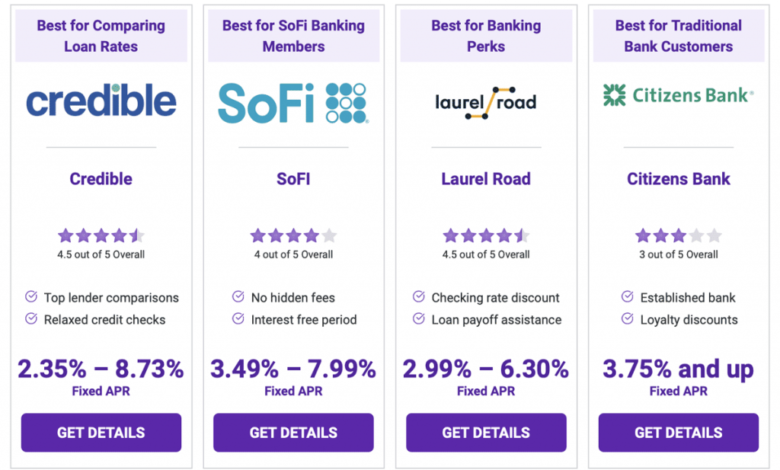

Credible

Best for Comparing Loan Rates

Key Features

- Compares rates from top lenders

- Flexible loan terms and monthly payments

- Variable APR as low as 1.86%

Credible is a loan marketplace that lets you fill out a single application to see pre-qualified rates from multiple lenders in one place. The marketplace looks at all kinds of loans, including student loan refinancing. You can compare options based on options that work for you, like monthly payments, variable or fixed rates, or time to repay. Once you choose an offer, you can finish your application and sign the agreement with the lender directly.

Credible

Variable APR

1.86% – 8.38%

Fixed APR

2.35% – 8.73%

Earnest

Best for Flexible Repayment Options

Key Features

- Defer one payment per year

- Biweekly auto-pay

- Loans serviced in-house

You can apply to refinance student loans with a balance of at least $5,000 with Earnest with a minimum credit score of 650. Unlike many online lenders, Earnest services loans in-house rather than through a servicing partner, and it offers flexible repayment options that could make repaying easier, like biweekly auto-pay and one deferred payment per year.

Earnest

Variable APR

Starting at 1.74%

Fixed APR

Starting at 2.74%

College Ave

Best for Flexible Repayment Terms

Key Features

- 11 loan term options between five and 15 years

- Fixed or variable interest rates

- Positive customer service reviews

College Ave is a mainstay in student loans and refinancing. Refinance loan amounts as low as $5,000 with loan terms at any interval between five and 15 years. That flexibility stands out against the competition, which usually offer designated terms of three, five, seven or maybe 10 years.

College Ave

Variable APR

3.44% – 6.64%

Fixed APR

3.49% – 6.74%

SoFI

Best for SoFi Banking Clients

Key Features

- No hidden fees

- Member perks

- No interest through Aug. 15, 2022

SoFi is a financial tech company with its roots in student loan refinancing, though it offers all types of loans and other financial services now. At its inception, it was a leader in refinance loans with no unnecessary fees. As a SoFi member, you can use perks that help you manage your finances, including discounts on other SoFi loans, invitations to live community events and access to SoFi’s banking and investing services.

SoFi

Variable APR

1.74% – 7.99%

Fixed APR

3.49% – 7.99%

LendKey

Best for Loan Reconnaissance

Key Features

- Loans serviced in-house

- Partners with community banks and credit unions

- Compare options from multiple lenders in one pla

LendKey is a student loan servicer and a platform for finding the best student loan and refinancing options from partner community banks and credit unions. LendKey’s platform streamlines the process, so you get the benefit of working with a community-oriented institution without the headache of multiple application processes.

LendKey

Variable APR

Starting at 2.14%

Fixed APR

Starting at 2.69%

Citizens Bank

Best for Traditional Bank Customers

Key Features

- Established financial institution

- Interest rate discount for Citizens Bank custome

- Repayment terms of five, seven, 10, 15 or 20 yea

Citizens Bank is an established financial institution with more than 40 years of experience providing student loan refinancing and other financial services. Choose among terms of five, seven, 10, 15 or 20 years to land on the rate and monthly payment that works for you. Citizens Bank customers can get an interest rate discount up to 0.25 percentage points.

Citizens Banks

Variable APR

Starting at 1.99%

Fixed APR

Starting at 3.75%

PNC

Best for Applying With a Cosigner

Key Features

- Large, established financial institution

- Student loans and refinancing options

- Cosigner release after 48 on-time payments

in financial services. Student loans and refinancing are among its vast services. The PNC Education Refinance Loan (PERL) is designed to help simplify student loan repayment, pay off loans faster and/or reduce your monthly payment.

PNC Bank

Variable APR

2.14% – 6.64%

Fixed APR

2.59% – 7.19%

Purefy

Best for Comparing Refinancing Rates

Key Features

- Platform specializes in student loan refinancing

- Refinance parent and student loans

- Compare and apply through one platform

Purefy is for anyone out of school, repaying student loans and looking for ways to save money. Use the platform to compare student loan refinancing options from multiple lenders side-by-side. The platform is free to use, and you can see prequalified rates in minutes. You can refinance private or federal loans through its partner lenders.

Purefy

Variable APR

1.74% – 7.24%

Fixed APR

2.43% – 7.94%

Sparrow

Best for Easy Repayment

Key Features

- Shop, apply and repay through one platform

- Compare offers from multiple lenders

- See real pre-qualified rates, not estimates

Sparrow is a platform for student loans, refinancing and repayment in one place. You can fill out a single application to see prequalified offers from multiple partner lenders for private student loans or refinancing. Then use the app to manage and automate repayment of your private and federal student loans in one place.

Sparrow

Variable APR

1.74% – 9.34%

Fixed APR

2.35% – 10.74%

Discover

Best for No Fees

Key Features

- No fees

- Refinance while you’re still in school

- 10- or 20-year terms

federal and private student loans. You’ll pay no application, origination or late fees. You can even refinance high-rate loans with Discover while you’re still in school. Repayment terms are either 10 or 20 years, depending on your credit.

Discover

Variable APR

2.49% – 6.49%

Fixed APR

3.49% – 7.99%

Splash Financial

Best for Refinancing Undergrad and Med School Loans

Key Features

- Compare offers from multiple lenders

- Exclusive interest rates from partners

- No application, origination or pre-payment fees

Splash Financial lets you compare options for several types of loans, including student loan refinancing. Compare offers with a single online application. In addition to its search function, Splash partners with its lenders to offer exclusive interest rates — with fixed rates as low as 1.99% — to help you get the best deal possible.

Splash Financial

Variable APR

1.74% – 8.70%

Fixed APR

1.99% – 8.63%

ISL Education Lending

Best for Graduated Repayment Plans

Key Features

- Refinance undergrad, medical, dental and parent

- Option for graduated repayment plans

- Terms of seven, 10, 15 or 20 years

ISL’s Reset Refinance Loan helps you pay off student loans with a potentially lower interest rate or better repayment terms. If your loan is eligible, you can opt for a graduated repayment plan, which will give you lower monthly payments upfront and gradually increase them over time. This costs more in interest overall, but could be useful for repaying private loans early in your career.

ISL Education Lending

Variable APR

n/a

Fixed APR

2.55% – 7.63%

Laurel Road

Best for Banking Perks

Key Features

- Refinance parent loans in your name

- Credit card with cash back toward loan repayment

- Discounts for Laurel Road Checking customers

Laurel Road is an online lender that offers specialized checking and credit card accounts designed to help you pay back student loans. When you open a Laurel Road Checking account, you get access to a lower interest rate on your refinance loan, and if you qualify for a Laurel Road Student Loan Cashback Card, you can earn cash back toward student loan repayment.

Laurel Road

Variable APR

1.89% – 6.20%

Fixed APR

2.99% – 6.30%

PenFed Credit Union

Best for Non-Profit Banking

Key Features

- No fees or pre-payment penalties

- Refinance student and parent loans

- Fixed interest rates

PenFed Credit Union is a non-profit financial institution serving members in all 50 states through online banking. It offers student loan refinancing with fixed rates between 4.49% and 6.68% and no hidden fees or pre-payment penalties. You don’t have to be a PenFed member to apply, but you’ll become a member if you accept a loan offer. It costs you nothing to be a member, and you’ll enjoy special discounts on an array of financial and other services.

PenFed Credit Union

Variable APR

n/a

Fixed APR

4.49% – 6.68%

What to Know Before Refinancing Your Student Loans

Refinancing your student loans can be a strategic way to reduce your costs and make repayment easier. But it comes with both benefits and drawbacks, so weigh both before turning over your loans.

Pros of Refinancing Student Loans

- Potentially lower interest rate.

- Potential for lower monthly payment and longer repayment period.

- Release co-signer from original loans.

- Replace multiple monthly payments with just one.

Cons of Refinancing Student Loans

- Losing federal borrower protections and repayment flexibility.

- New credit request on credit report makes a temporary mark.

- Might come with upfront fees.

The greatest potential downside to student loan refinancing applies to borrowers with federal student loans. Refinancing or consolidating federal student loan debt in any way other than a Direct Consolidation Loan from the Department of Education shifts your obligation to a private company.

That means you no longer have any of the benefits that come with federal student loans, including income-driven repayment plans, forgiveness, cancellation or flexible deferment options.

That drawback doesn’t apply if you already have private loans — you can refinance and move your loans among private companies without serious risk. But check the options of your current loan before replacing it to make sure you’re not giving up flexible repayment options you might need in the future.

How to Refinance Student Loans

You can refinance any student loans with private lenders like those listed above. But there are a few additional steps to take before refinancing federal loans to make sure you’re choosing the best option for your financial situation.

Refinance Federal Student Loans

You might have several student loans to your name, even though you only applied once and may have received money as a lump sum each semester. You can simplify repayment and refinancing by first combining all of your loans into a Direct Consolidation Loan, a student loan consolidation option that creates one balance and one monthly payment, and sets the interest rate at the average of all the loans.

If you want to reduce your interest rate — and you’re confident in your resources to stay on top of repayment — you can refinance your federal loan with a private refinancing option.

Before refinancing a federal loan with a private lender, consider these questions:

- Are you in a profession that’s eligible for forgiveness after a period? A private loan won’t be forgiven.

- Do you expect a stable (or growing) income for the next five or 10 years? Flexible repayment options with federal loans could protect you in case of volatile or uncertain income in the future.

- Can you get a lower interest rate with a private loan? This is the biggest benefit to move from federal to private — without it, the benefits of federal loans far outweigh those of private loans.

Refinance Private Student Loans

Refinancing private student loans is as simple as — or even easier than — taking out a private loan in the first place.

If your financial situation improves, student loan refinancing could help you get a lower interest rate, lower monthly payment or both. You could save hundreds or thousands of dollars in the long run.

You could also try refinancing if you’re having trouble repaying private loans. A lender might offer a longer repayment period with lower monthly payments that’ll fit more easily into your overall financial plan.

Steps to Refinance Student Loans

Whether you’ve got federal or private student loans, follow these steps to refinance:

-

- Note any must-haves about your current repayment plan, like income-driven repayment, interest, terms, or options for forgiveness or deferment. Look for those in new loan offers.

- Apply for pre-qualified rates with an online lender or marketplace. You’ll see interest rates, monthly payments and terms you could qualify for. A marketplace lets you see offers from several lenders at once.

- Choose a lender, and officially apply. Fill out the full application to apply for the loan.

- Accept an offer and set up a payment plan. If eligible, a lender will make you a loan offer, and you can choose to accept it and take the loan. You’ll also be able to set up a payment plan, including opting into automatic payments.

- Pay off existing loans. In most cases, a student loan refinancing company will pay off your existing loans directly.

- Repay the loan. Use auto-pay or set monthly reminders to make your payments, so you avoid late fees and unnecessary interest. Stay abreast of your lender’s repayment options, so you can adjust if you need to skip or defer a payment in the future. If your lender offers income-based repayment, you’ll likely have to report your income once a year and more often if it changes.

Loan Refinancing Costs to Consider

The main benefit to student loan refinancing is the potential to save money. Make sure you don’t accept a loan offer that eats up those savings in unexpected fees!

Before you accept an offer, review the agreement carefully and look for these common costs:

- Interest: Note the annual percentage rate (APR) listed for the loan. It can be fixed or variable. Variable rates usually come with a lower base rate but will change with the prime rate. Fixed rates stay the same for the life of your loan, so you know exactly what you’ll pay into the future. Look for an interest rate that’ll save you money in the long run compared to what you’re paying now.

- Origination fee: This isn’t common for student loan companies, but some lenders charge a fee upfront when you receive your loan. Origination fees are usually around 2% or 3% of the loan amount and come out of the amount disbursed to your current lenders.

- Late fee: Most loans you take out will include a fee for late payments, usually a percentage of the payment due. Many student loan lenders are doing away with late fees and building in options for flexible repayment, so look for options that skip this fee.

Can You Refinance If You Had a Cosigner?

If you took out private student loans originally, you might have used a creditworthy cosigner like a parent, relative or family friend. They remain responsible for the loans until they’re paid off.

Some private student loans come with an option for cosigner release after around 12 to 18 months of on-time payments, as long as you have the credit and income to qualify to take on the loan yourself. If your loan didn’t come with a cosigner release option, you could release them by refinancing, instead.

Refinancing pays off the old loan, so the cosigner will no longer be responsible for the debt. As long as you can qualify for a new loan on your own, you don’t have to involve the cosigner anymore.

Frequently Asked Questions (FAQs) About Student Loan Refinancing

We’ve rounded up the answers to some of the most common questions about where to refinance student loans.

Is It Worth It to Refinance a Student Loan?

Refinancing usually is NOT worth it if you have federal loans that could qualify for forgiveness or cancellation. In other cases, student loan refinancing should get you a lower interest rate than your existing loans. The savings that comes with lower interest is the main benefit of refinancing. But refinancing could also be worth it for you if you’re having trouble keeping up with monthly payments for existing private student loans — you might get a lower monthly payment, even if you don’t get a lower interest rate.

When Is a Good Time to Refinance Your Student Loans?

Struggling to keep up with monthly payments is NOT a good reason to refinance federal student loans — look into income-driven repayment plans instead so you can maintain repayment flexibility and borrower protections. To qualify for a lower interest rate, apply to refinance when your financial situation, income and credit history are better than they were when you took out the original loan. You should be in a position to look more creditworthy to lenders and be comfortable keeping up with the monthly payments for the next five to 10 years.

Is It Cheaper to Refinance Student Loans?

Student loan refinancing could save you money if you get a lower interest rate than you’re paying on your current loans. Lower interest could save you hundreds or thousands of dollars over the life of the loan and keep your monthly payments lower.

Can You Refinance Student Loans for Free?

Most student loan lenders offer student loan refinancing without an upfront fee, though some charge an origination fee of 2% or 3% of the loan amount. Once you get the new loan, you’ll have to make new monthly payments, and your balance will accrue interest at your new rate.

Does Refinancing Student Loans Hurt Your Credit?

Refinancing student loans shouldn’t hurt your credit as long as you repay on time. Seeing pre-qualified rates won’t affect your score at all, and applying for a loan will only ding your credit score temporarily. Refinancing into a loan you have trouble repaying could be bad for your credit score through late payments and debts in forbearance.

Contributor Dana Miranda is a Certified Educator in Personal Finance® who has written about work and money for publications including Forbes, The New York Times, CNBC, Insider, NextAdvisor and Inc. Magazine.

[ad_2]