[ad_1]

The credit score: a deceptively simple three-digit number that can dictate or impact your financial life in a variety of meaningful ways, from being able to rent a home or open a utility account to whether or not you are approved for a credit card or which mortgage rate you qualify for. Given their importance in the American financial system, it makes sense that understanding and improving your credit score is a goal for many. But it’s easy to get intimidated or disheartened by what can seem like wide discrepancies or inexplicable changes in that score. What drives this? Let’s dig in a little to break down differences in your credit scores and why they exist.

Contents

NO ONE CORRECT SCORE

First, crucially: contrary to what many believe, there is no ONE, individual correct credit score for an individual. Everyone has a variety of different scores at any given time, given the many different factors that make up your various scores. Let’s break down the different components that can affect your credit score, the credit bureau data, the credit scoring model and version, and how your score gets updated.

The credit bureau data being utilized

Behind every credit score is a credit report, a set of historical data on your past credit and lending activity. This includes credit accounts (both open and closed), your payment history for each, and any negative marks, which could include late or missed payments, collections, or charged-off and closed accounts. The three main providers of credit reports in the US are Experian, Equifax, and TransUnion.

While many customers may see their credit reports looking quite similar across the three bureaus, they can differ. If past lenders have sent your application, account, or payment data to only one or two of the three main bureaus, that data may differ in a way that could meaningfully impact your score.

You can access your TransUnion credit report for free on Mint, as well as being entitled to one free credit report per bureau per year via www.annualcreditreport.com.

The credit score model

A credit score model applies an algorithm to the underlying credit report data, resulting in that famous three-digit score. There are two main credit score models currently widely available in the US: FICO and VantageScore. We’ll dig into the major differences below in just a minute!

The model version

Adding to the complexity, both major model providers have different versions of their scoring models, which can significantly impact the score output!

FICO offers different models for mortgage, auto, and credit decisions. For the credit versions, which lenders are likely to use for products like credit cards and personal loans, the most recent model version is FICO Score 9.

VantageScore recently rolled out VantageScore 4.0, following its successful 3.0 model.

The dates of recent updates

Lastly, the date(s) on which your lenders send updates to the credit bureaus, as well as the dates on which your score is refreshed, can impact your score temporarily. A credit score, at least for now, is a point-in-time snapshot of your credit risk versus a real-time update.

Generally, lenders send an update with your outstanding balance and updated payment record to the credit bureaus about once every ~30 days. Imagine you do a bunch of holiday shopping one day and nearly max out your credit card, and the next day your lender updates the bureaus with your high balance. Your next credit score update may drop due to higher utilization, even if you paid it off a few days later. Not to worry: this should be resolved with the next update after your balance is paid off.

Additionally, the date your credit score is updated will impact whether or not recently received updates have yet to be factored into your score.

In summary: your score can fluctuate, sometimes significantly depending on your available credit and your balances/outstanding debt at the point in time that updates are sent to the lender. Making multiple payments per month, especially after large purchases, can help reduce these swings.

Now that you understand why it’s possible to have a large variety of credit scores at once, let’s dig into the differences between the main models.

WHAT IS THE VANTAGESCORE MODEL?

The VantageScore model was founded in 2006 in partnership between the three major credit bureaus, with the goal of introducing competition to the credit score market and expanding access to credit for consumers underserved by traditional credit models. While the new VantageScore 4.0 just rolled out, Mint, Credit Karma, and many other companies are providing millions of consumers with access to their free TransUnion 3.0 credit score.

The main factors in your VantageScore 3.0 credit score are:

- Payment history: about 40%

- Credit age and mix: about 21%

- Credit utilization: about 20%

- Balances: about 11%

- Recent credit applications: about 5%

- Available credit: about 3%

DIFFERENCES FROM FICO

There are many similarities between the VantageScore and FICO scoring models. Both score consumers on a 300-850 scale, and both place the highest importance on payment history and credit utilization as the strongest predictors of credit risk.

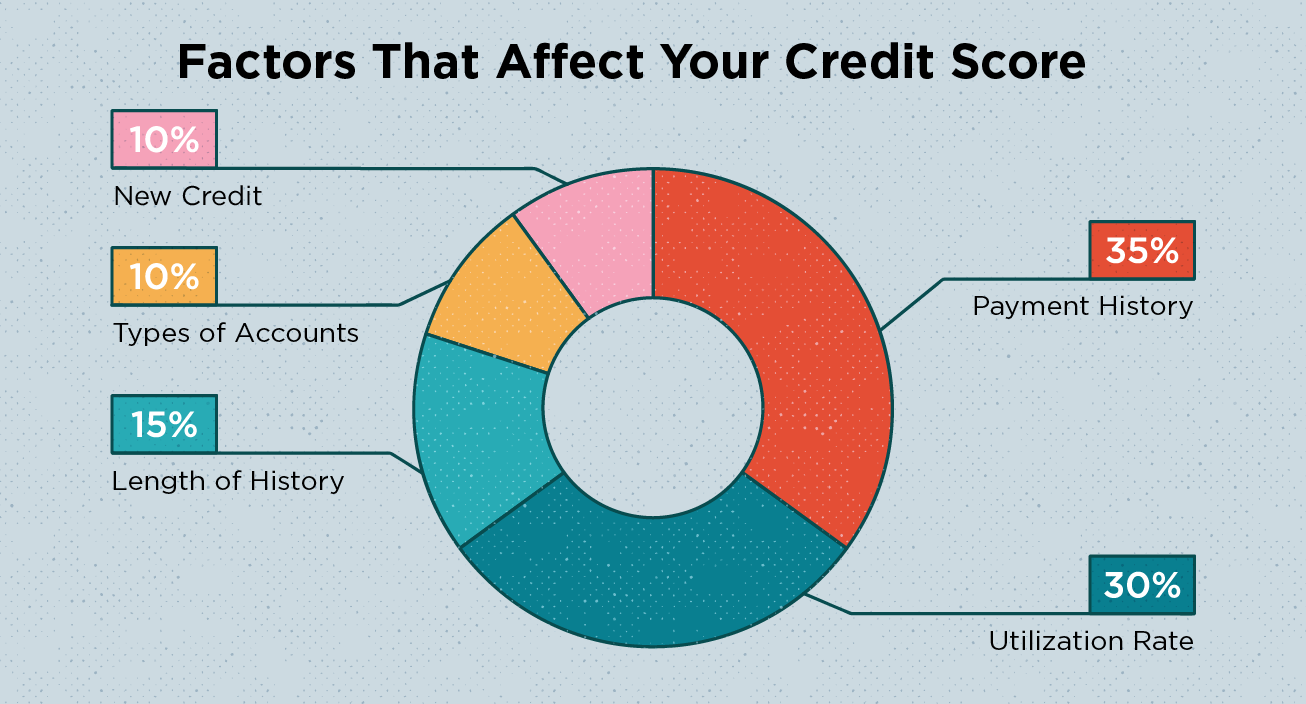

In general, FICO credit models group your credit report data into five categories, with the following weight:

- Payment history (35%)

- Amounts owed (30%)

- Length of credit history (15%)

- New credit (10%)

- Credit mix (10%)

While the components of both credit scoring models are similar, the weighting differs slightly, along with some other aspects of the score. Those with limited credit history may find that they don’t have a FICO score, but do have a VantageScore: while FICO requires six months of credit history to establish a score, a VantageScore may be generated with as little as one month of data.

For those who have accounts formerly in collections that have been paid off in full, VantageScore will prove more forgiving: VantageScore ignores paid off accounts in collections in the computed credit score, unlike most versions of the FICO scoring models. The newest model, FICO 9, will similarly be ignoring those paid-off accounts.

SUMMARY

While credit scores – and, specifically, the numerous different scores you may encounter – can be confusing, they are an incredibly helpful tool to understand your own financial health and indicators that may play a role in determining whether you will be granted access to new credit from a lender. As securing credit can play a major role in significant life goals for many people, whether buying a car, a home, or financing education, it’s important to understand your score and how you can improve it. To see your score on Mint and receive personalized insights take a look here!

Related

[ad_2]